How Capital Gains are Taxed in Canada

Written by Tiffany Woodfield, CRPC®, CIM® Associate Portfolio Manager

It is important to understand how capital gains are taxed in Canada and to be able to utilize capital losses. As a taxpayer, you will realize a capital gain when you get rid of capital property if the amount of the disposition is more than the adjusted cost base for the property.

What does that mean in plain English?

It means that when you sell a property or investment for more than you initially paid, you'll have realized a capital gain. When you know how capital gains work in Canada and how you will be taxed, you can prevent excess taxation.

Nobody likes to pay more tax than they need to, especially when selling a property, so let's review how capital gains are taxed in Canada.

Please note that the information in this article is general. You should consult a tax professional about your situation.

TABLE OF CONTENTS

- History of Capital Gains Tax in Canada

- How To Calculate Capital Gains Tax In Canada

- Calculation of Capital Gains and Capital Losses

- Lifetime Capital Gains Exemption

- Tax on Death or Deemed Disposition

- How To Avoid or Reduce Capital Gains Tax In Canada

- How To Defer Capital Gains Tax In Canada

- Capital Gains Tax In Canada On Real Estate

- Capital Gains Tax In Canada On Stocks

- Capital Gains Tax In Canada For Non-Residents

- Reinvesting Capital Gains From Real Estate in Canada

- Capital Gains Tax On Second Property In Canada

- Short and Long Term Capital Gains Tax Canada

- Common Questions about Capital Gains Tax in Canada

- Summary of Key Points

History of Capital Gains Tax in Canada

Taxation of capital gains was first introduced to Canada in 1972. Before that, capital gains were tax-free. The capital gains tax was brought in to replace inheritance taxes. Whereas, in the US, capital gains tax has been around since 1862 to help finance the Civil War.

How To Calculate Capital Gains Tax In Canada

To calculate capital gains in Canada, you first determine if the loss or gain from getting rid of the property is an income transaction or a capital transaction. To help understand this concept, it is common to think of "the tree or the fruit."

In other words, it is a capital property if the tree was acquired to reap the fruit of the tree. For example, if you purchase a condo to earn rental income, it is capital property. Thus only 50% of the capital gain is taxable. In addition, property that is held for personal use is usually considered to be capital property.

However, it is an income transaction if you purchase several condos within a short time frame and flip them to earn income from the resale. Thus, all of the capital gain is taxable, and you won't have a 50% tax-free portion.

Thus, you and your accountant need to determine your intention at the time of purchase.

Calculation of Capital Gains and Capital Losses:

As mentioned, in Canada, the capital gain is the proceeds from the sale, less the adjusted cost base. As of 2022, the taxable capital gain is 50% of the total capital gain, and the capital loss is the adjusted cost based less the amount of the sale.

The allowable capital loss, which reduces the taxable capital gain, is 50% of the capital loss.

Consider the following examples:

Capital Gain on Shares of Butterball Ltd.

Amount of sale $100,000

Less the cost of sale $5000

Less the adjusted cost base* $30,000 ($35,000)

Capital Gain or Capital Loss $65,000

Taxable capital gain (half of 65,000) $32,500

So $32,500 would be added to your income and taxed at your marginal rate for the year.

*The adjusted cost base is the original purchase price plus any costs to purchase the property such as commissions, land transfer taxes and brokerage fees. Major repairs and renovations may be added to the property's adjusted cost base.

Capital Loss on Shares on West Ltd.

Amount of sale $30,000

Less the cost of sale $5000

Less the adjusted cost based $30,000 ($35,000)

Capital gain or capital loss ($5,000)

Allowable capital loss ($2,500)

In this example of a capital loss, you paid $30,000 for a property and $5000 in expenses. But you only sold the property for $30,000. Thus, you have a capital loss of $5000. So $2,500 (50% of the capital loss) can be used to offset taxable capital gains.

You cannot deduct a capital loss from income in the year of sale. Still, you can use it to offset taxable capital gains for three years prior or any future taxable year. The exception to this rule is in the year of death and the year before the taxpayer's death where allowable capital losses can be deducted from any income, not just capital gains.

Lifetime Capital Gains Exemption

There are two situations where the gain on the sale of a property may not face tax in Canada.

Principle Residence Exemption (PRE)

The principal residence exemption means any gain from the sale of your principal residence will not be subject to a capital gain tax.* The principal residence definition states that a property is ordinarily inhabited, but there is no requirement that it is used as a residence more than any other residence. This definition creates a little flexibility for tax planning with your accountant.

The formula for calculating principal residence is a one plus formula that allows taxpayers to shelter their gains when they sell and purchase another residence within the same year.

The procedure is an election for the property for each year it was owned. When you have more than one property that can qualify, choosing the property with the most significant gain per year typically makes the most sense.

Proceeds of disposition x 1 + number of years designated as a principal residence

Number of years owned

Tax on Death or Deemed Disposition

There are situations which may trigger what is called a deemed disposition. A deemed disposition is when a taxpayer's property, such as a home or investments, is treated as if it were sold regardless if it is actually sold or not. When a deemed disposition is triggered, you or your estate will have to pay the capital gains taxes.

Here are some circumstances where a deemed disposition may be triggered:

- Immediately before the death of the taxpayer

- When the use of the property changes from business use to personal use or the other way around

- When a taxpayer moves and therefore stops being a resident of Canada

- When a taxpayer disposes of property by way of a gift

Whether there is a deemed disposition or an actual disposition of capital property, you must calculate whether there is a capital gain or capital loss. Please note that there are cases where there is a deemed disposition for tax purposes, but it could take place on a rollover basis. Keep reading this article for more information on rollovers.

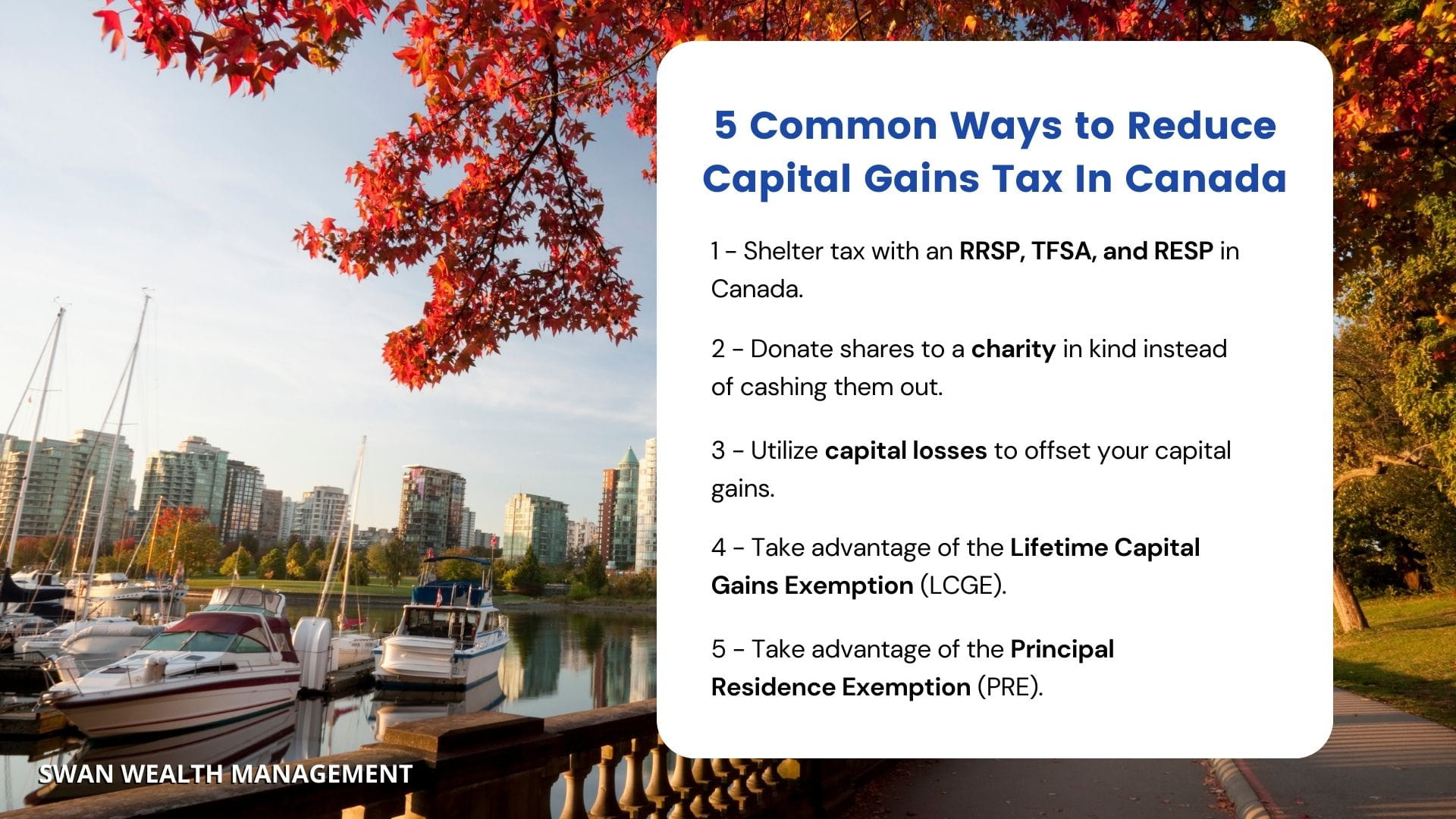

How To Avoid or Reduce Capital Gains Tax In Canada

While you cannot avoid "death and taxes," you can reduce your taxes by utilizing a few different planning strategies. Below are a few strategies you can use to minimize capital gains tax in Canada.

1) You could shelter tax and capital gains by funding an RRSP, TFSA and RESP in Canada. Each has various funding rules and requirements but are a great way to save money and taxes.

2) You could donate shares to a charity in kind. Rather than cashing out the shares, you would donate them in their original form.

3) You could utilize capital losses to offset your capital gains. For example, suppose you have $1000 in a taxable capital gain from selling one stock, but you have $1000 in allowable capital losses from selling a different stock. You could use those capital losses to offset your gains. Thus, your net capital tax on this sale would effectively be zero.

4) To reduce tax, you can carry forward allowable capital losses into future years. And you can carry them back for three years.

5) You may choose to take advantage of the Lifetime Capital Gains Exemption (LCGE) and Principal Residence Exemption (PRE).

6) When transferring property or a business to a family, you might be able to spread the capital gains over a few years to take advantage of progressive tax rates. There are rules you must follow to do this. You must claim at least 20%—or the payment amount—over a maximum of 5 years. You would also need to be prepared to have the payments spread out.

*You should speak to a tax professional about how to do any of these strategies.

How To Defer Capital Gains Tax In Canada

One way to defer capital gains is by using a rollover.

With a rollover, the property is transferred from one person to another (or to a trust or corporation). The proceeds are the adjusted cost base of the person transferring the property.

Rollovers for capital property are available with a transfer to the following:

- qualified spousal trust

- spouse or common-law partner

- alter ego trust

- joint partner trust

- spouse from a settlement of rights

- intergenerational transfer of farm or fishing property

- corporation in exchange for shares after filing an ss.85 election

- Canadian resident beneficiary due to a capital interest in a trust

Make sure you speak to your accountant if you plan on using a rollover. And review this article from the CRA on how to calculate the capital gains deferral.

Capital Gains Tax In Canada On Real Estate

As Canadian residents, many people have seen a tremendous increase in the value of their principal residence.

In Canada, you usually do not owe tax on the capital gain from the sale of your principal residence because of the PRE exemption. However, this is not the case in the US. If you are a US citizen living in Canada, you still have to report the capital gain to the US and may owe tax to the IRS.

One property per family can be claimed as a personal residence in a single year. A family unit includes a spouse, common-law partner and children under 18 living in the home.

Capital Gains Tax In Canada On Stocks

In Canada, 50% of your gain from the sale of a stock will be included as income and taxed at your marginal tax rate.

Here's an example to clarify what this means in real life:

Imagine you own stock that you purchased for $5000. When you sell it, you receive $8,000. Thus, the total capital gain is $3,000. Because 50% of the gain must be included as income, your taxable capital gain is $1,500.

In this case, it is like you earned $1,500 in income, and this "income" will be taxed at your marginal rate. If you are in the highest marginal rate in BC, your combined federal and provincial tax rate is 53.5%. Thus, on $1,500, you will owe $802.5 in tax.

Keep in mind that $802.50 in tax is on a total gain of $3000. If you do the math, you'll have paid around 27% tax on the $3000 of earnings from the sale.

As you can see, capital gains are taxed favourably in Canada, especially when compared to interest income.

For example, when you purchase a guaranteed investment certificate (GIC) you earn interest income. Consider the example from above but with $3000 in gains from interest. This interest income would all be taxed at your marginal rate. If you're in BC's highest tax bracket, your marginal rate would be 53.5%. Thus, you would pay $1605 in tax on the $3000 of interest income.

Capital Gains Tax In Canada For Non Residents

Canada taxes are based on residency. When you are a non-resident of Canada, you are only liable for Canadian tax on income from Canadian sources.

Traditionally there isn't a non-resident withholding tax on capital gains. But there is a withholding tax when selling Canadian real estate. Think of withholding tax as the final tax obligation to Canada on this income.

Usually, a non-resident of Canada won't be required to file a Canadian income tax return as long as the non-resident withholding tax is withheld. The usual withholding tax rate is 25%, but the Income Tax Treaty usually provides a reduced rate of withholding taxes.

You should speak to your cross-border accountant and financial advisor to ensure you understand what rate will be withheld on your investments and/or the sale of Canadian property.

Reinvesting Capital Gains From Real Estate in Canada

People often ask about reinvesting capital gains from real estate when dealing with rental properties. Individuals and associations are often looking for the opportunity to defer the capital gains on the sale of a rental property by using those funds to purchase another rental property within 12 months.

However, currently, this is not allowed. Moreover, because a rental property is not your principal residence, the rules of regular taxable capital gains apply.

Capital Gains Tax On Second Property In Canada

Remember that the one residence you choose to claim as your principal residence just needs to be the one you "ordinarily inhabited."

Many Canadians claim the residence with the largest capital gain per year to be their principal residence to make the most of the Principal Residence Exemption. The CRA can challenge your exemption claim, so make sure you work with your accountant to do this properly.

While you may not owe capital gains tax on your principal residence, you will be taxed on the capital gain of your second property. As with other capital gains in Canada, 50% of your capital gain will be taxed at your marginal tax rate.

Short and Long Term Capital Gains Tax Canada

In the US, you are usually taxed at the same rate as your ordinary income if it is a short-term capital gain. In contrast, long-term gains are typically taxed at a much lower rate than your ordinary tax rate.

In Canada, we do not measure short-term and long-term capital gains. Instead, the formula is that 50% of the capital gain is taxable. Whether the capital gain happened in the short or long term is not relevant in Canada.

Common Questions about Capital Gains Tax in Canada

Can you defer capital gains tax in Canada?

There are some ways to defer capital gains tax in Canada. Depending on your situation, you may be eligible to do a rollover.

How are capital gains taxed in a corporation in Canada?

Investment income in a Canadian-controlled private corporation is usually considered passive investment income. The passive investment income rate in corporations is 50%. For capital gains, this means 50% of the capital gain is taxable, and it is taxable at 50%.

When the passive income in a corporation exceeds $50,000, the business pays a higher tax rate on some of its earnings. In other words, when passive income exceeds $50,000, a corporation has less access to the small-business tax rate.

It is essential to speak to your accountant about your particular situation.

In addition, if you are a US person living in Canada and investing in a corporation, there are additional complexities not mentioned in this article. You should speak with a cross-border accountant and cross-border financial advisor about your situation.

What percent is capital gains tax in Canada?

There isn't a fixed tax rate for capital gains tax in Canada. Instead, 50% of your total capital gain is taxable at your marginal tax rate, which varies depending on your province and income level.

How do I avoid capital gains tax in Canada?

You can't avoid paying tax on your capital gains in Canada. However, you can use various planning strategies to reduce your tax bill. You may use capital losses to offset the capital gain, reducing your tax bill. Some people use tax-loss harvesting, which means selling off poor-performing investments to offset the gains on the winners. However, you must remember that CRA is strict on investors who create a "superficial loss." For example, if you were to sell a low-performing stock, only to purchase it back within 30 days, the CRA would not look favourably upon this.

Another strategy to offset capital gains is to donate stocks "in kind" to a charity rather than donating cash. You avoid the capital gains tax when you donate the stock in a capital gain position. You also get a tax receipt if you donate it to a registered charitable institution.

In addition, you could utilize the principle residence exemption (PRE) and the Lifetime Capital Gains Exemption (LCGE) if eligible.

With any of these strategies, you must consult a tax professional about your situation.

How much tax do Canadians pay on capital gains?

The amount of tax Canadians pay on capital gains varies. Your income level and your province will determine your marginal tax rate. 50% of your capital gains are added to your income and taxed at your marginal rate.

How does Canadian capital gains tax work?

Capital gains are taxed favourably in Canada compared to interest income or dividend income. Only 50% of your capital gain is added to your income and taxed at your marginal rate.

Summary of Key Points:

- There isn't a specific tax rate on all capital gains in Canada. Instead, 50% of a capital gain is taxable at your marginal rate for the year.

- When it comes to capital gains in Canada, there are a lot of planning opportunities available to Canadian residents.

- In Canada, the tax on capital gains isn't based on whether the gain is short-term or long-term as it is in the US.

- Speak to a professional accountant to get advice on your particular situation.

Next Steps

If you’re a Canadian resident or are planning on moving to Canada and need assistance with moving and optimizing your investments, estate planning, wealth management and portfolio management, please get in touch. At SWAN Wealth, we specialize in Canadian financial planning, cross-border financial planning and cross-border wealth management.

More Canadian Financial Planning Articles & Guides

If you’re planning a cross-border move, these articles and guides will help you simplify your move and ensure you’ve covered everything.

💠 Retirement Planning in Canada

💠 How to Reduce Taxes for High Income Earners in Canada

💠 Cross-Border Estate Planning Guide

💠 Financial and Tax Planning for US Citizens Living in Canada

💠 Canadian RRSP Facts for Dual Citizens, Expats and Canadians

About the Author

Tiffany Woodfield is an Associate Portfolio Manager licensed in Canada and the USA, and the co-founder of SWAN Wealth Management, along with her husband, John Woodfield. Tiffany advises clients who live in Canada and the United States and want to simplify their cross-border financial plan, move their assets across the border, and optimize their investments to minimize their tax burden. Together Tiffany and John Woodfield help their clients simplify their cross-border finances and create long-term revenue streams that will keep their assets safe whether they live in Canada or the US.

Schedule a Call

Book a 15-minute introductory call with SWAN Wealth Management. Click here to schedule a call.

![]()