Roth IRA Canada How to Manage Your Investments Across the Border

Written by Tiffany Woodfield, CRPC®, CIM®, TEP®

Reading Time: 7 minutes 30 seconds.

If you live in Canada and have a Roth IRA, you may be wondering what to do. Likewise, if you're planning on retiring to Canada from the US, you may be wondering how to manage your Roth IRA.

Can you keep it? If so, how can you manage it properly?

This blog discusses the main things you need to consider if you have a Roth IRA and you are planning a cross-border move.

Please note this article is not intended to provide tax or legal advice. Do consult with a qualified cross-border accountant to understand your particular circumstances before acting on any of this information.

Table of Contents:

- Your Roth IRA in Canada - How to Manage

- Roth IRA Treaty Election Filings

- When to File a One-Time Treaty Election

- Should you transfer your 401(k) to a Roth IRA?

- Who can do a Roth IRA Conversion?

- Consider This One Thing Before Doing a Roth IRA Conversion

- Are Roth IRAs taxed in Canada?

- Roth IRA Minimum Distributions

- US-Canada Tax Treaty

- Can You Make Canadian Contributions?

- Managing Your IRA with a Dual-Licensed Financial Advisor

- What is the Canadian Equivalent of a Roth IRA?

- Summary

Your Roth IRA in Canada — How should you manage your investments?

First, be assured that you do not need to liquidate your Roth IRA when you move to Canada. The restrictions around non US resident held IRAs and Roth IRAs are being enforced more strictly, but that doesn't mean you need to worry. While your US brokerage firm may not be able to manage your IRA legally if you move across the border, there is a solution.

The best solution may be to work with a dual-licensed advisor. A dual-licensed financial advisor is licensed and regulated in both Canada and the US. This means they can manage IRAs and 401(k)s whether you live in Canada or the US. A dual-licensed financial advisor can also provide insights on what investments to avoid. Some common investments may cause a surprise tax hit for a US person living in Canada. If you're like many of my clients, then avoiding unnecessary taxes is a priority.

Roth IRA Treaty Election Filing and Contributions

As a Canadian Resident, if you contribute to your Roth IRA, there may be some tax issues. If you contribute to your Roth IRA as a Canadian resident you will “contaminate” your Roth and may lose the tax-free growth for Canadian tax purposes. Also, you must file a one-time treaty election by the filing date, which is April 30th of the year after you become a resident in Canada to keep the tax-free growth. In other words, if you don't file the correct paperwork on time, you may face a tax hit. Working with a cross-border accountant and financial advisor will help you stay on top of the necessary paperwork.

Please speak to a qualified professional tax advisor to discuss your situation.

Government of Canada information on taxation of Roth IRAs

When to File a One-Time Treaty Election

To keep your Roth IRA from being exempt from Canada and US tax, you must file a one-time Treaty Election for each Roth IRA account. You must do this by the filing deadline for every Roth IRA account that you hold.

This deadline is the same filing due date as your due date for your first personal tax return of the first year of residence in Canada. That date is April 30th of the year after you become a resident.

Your cross-border tax accountant can help you file the Treaty Election form.

Click here for the government of Canada information on the taxation of a Roth IRA.

Should you transfer your 401(k) to a Roth IRA if you're moving to Canada?

There are advantages and disadvantages to both a 401(k) and an IRA. A 401(k) has the following benefits:

- A 401(k) offers creditor protection.

- A 401(k) may have a lower cost.

- Certain 10% penalty exceptions such as first-time home purchase or qualified higher education expenses, are only available for plan withdrawals.

While an IRA has other benefits, which include the following:

- An IRA generally has a broader selection of investment options.

- An IRA allows you to consolidate funds.

- An IRA offers more flexible distribution options.

There are some important tax considerations when converting a 401(k) to a Roth IRA. The amount you convert to a Roth IRA will be taxable in the year you convert. If you think your tax rates will increase, then perhaps you will decide to convert your 401(k) to a Roth IRA.

More commonly, you will need to rollover your 401(k) to an IRA. Then you will convert the IRA to a Roth IRA. Also, you usually will need to be separated from your employer before you can rollover a 401(k) to a Roth IRA.

Who can do a Roth IRA conversion?

Anyone can convert their IRA to a Roth IRA. There are no age limits, income limits, or a requirement to be employed or working. Often people do a Roth IRA conversion to hedge against an increase in future tax rates. For example, suppose you were to move to Canada, where tax rates are higher. In that case, you might hedge against those increased tax rates by doing a Roth IRA conversion.

If you do a Roth IRA conversion, remember you will be stuck with your conversion. So if the tax bill is higher than you thought or you change your mind, you cannot go back to an IRA. The amount that is converted from an IRA to a Roth IRA is generally added to your income, and you will need to report it on your tax return for that year.

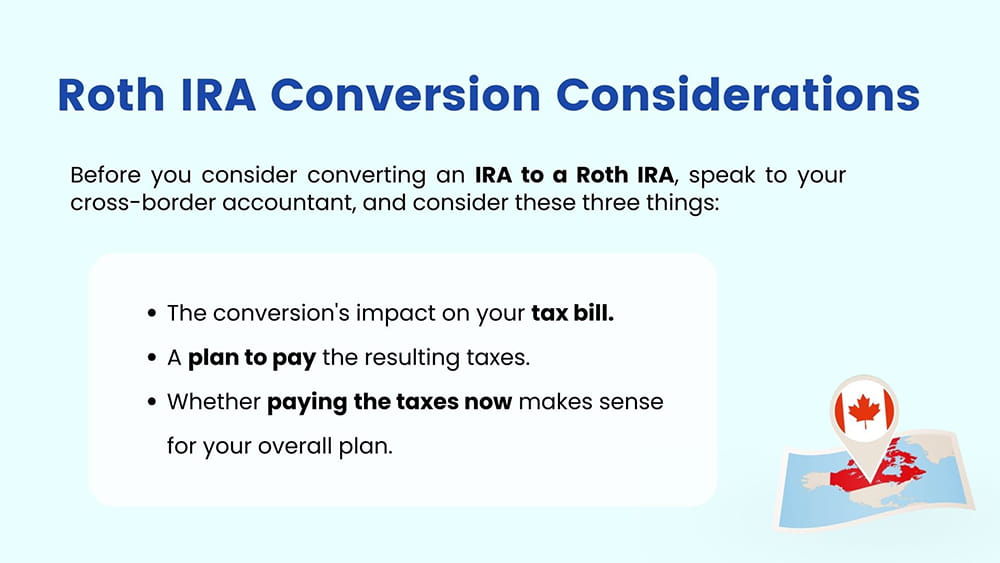

Consider the Following Before Doing a Roth IRA Conversion

Before you consider converting an IRA to a Roth IRA, speak to your cross-border accountant and consider these three things:

- The conversion's impact on your tax bill

- A plan to pay the resulting taxes

- Whether the benefits of paying the taxes now vs. at a later date makes sense for your overall plan

Also, note that a Roth IRA conversion is usually not recommended once you are a Canada tax resident. This is because you will be subject to tax in Canada, meaning it may cost you more tax to do the Roth IRA conversion after moving.

Are Roth IRAs taxed in Canada?

This tax information has been reviewed by Heather Sanders, CPA, CA of Tax Junction.

If the correct rules are followed, Roth IRAs may not be taxed in Canada. Remember that you need to follow the US rules. One rule is that you must hold a Roth account for at least five years and be over the age of 59.5, or you may be subject to penalties and US federal taxation.

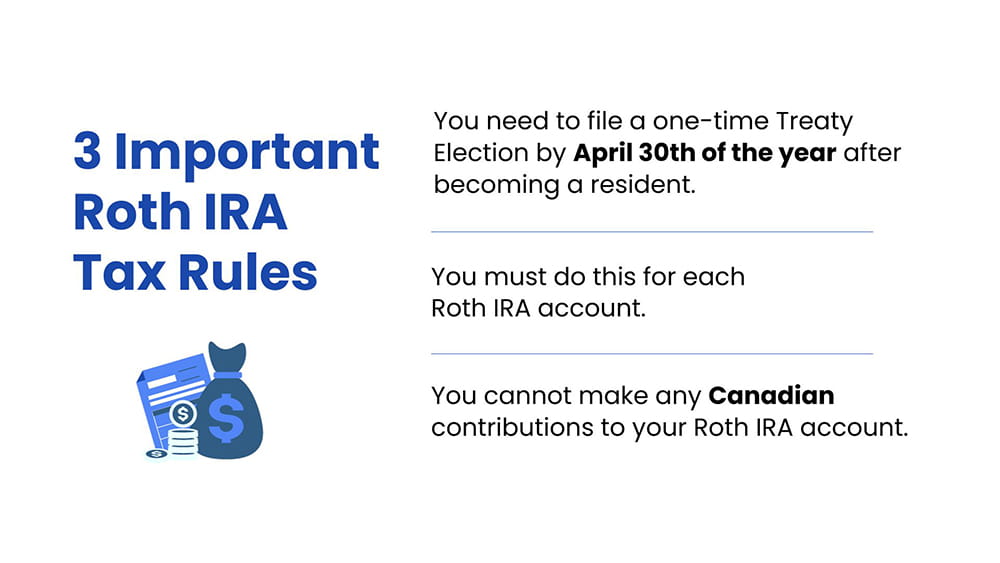

There are two critical rules around Roth IRAs when you become a Canadian resident:

- You need to file a one-time Treaty Election by April 30th of the year after becoming a resident. You must do this for each Roth IRA account.

- You cannot make any Canadian contributions to your Roth IRA account.

If you follow these Canadian rules and would be exempt from US tax if you were a US resident, you may be exempt from Canadian taxation.

However, please note that if a Treaty Election is not filed, the income accrued in the Roth IRA will need to be reported on your tax return. This will be taxable annually.

Please note that you should speak to a qualified professional tax advisor to discuss your situation. There may be further specifics you need to take into account.

Roth IRA Minimum Distributions

If you are the Roth IRA owner, there are no required minimum distributions during your lifetime. But if the Roth IRA is inherited, there are required distributions. With certain exceptions, if the Roth IRA is inherited, non-spouse beneficiaries will need to take out distributions and liquidate the account within ten years.

How does the US-Canada Tax Treaty come into play?

The US-Canada Tax Treaty treats Roth IRAs held by Canadians or Canadian Residents as a pension as long as a valid Treaty Election is filed. Also, there must be no contributions made once you are a Canadian resident.

Can You Make a Canadian Contribution to a Roth IRA?

I wouldn't advise any of my clients to make a Canadian contribution to a Roth IRA. If you do so, you may lose the tax-deferred status for your Canadian taxes. In other words, you may end up paying tax on your Roth IRA in Canada.

A rollover Roth IRA or Inherited Roth IRA may be considered a Canadian contribution depending on the circumstance—particularly if a Treaty Election isn't made. This includes if you converted an IRA or 401(k) and deposited the funds into the Roth IRA while you were a resident in Canada. You must speak to a cross-border accountant before you consider making a contribution.

Manage Your IRA with a Dual-Licensed Financial Advisor

The main benefit of working with a dual-licensed financial advisor is that you can keep your US retirement accounts intact. You will not be forced to convert or close them. This is important as it helps you avoid a surprise tax hit.

A dual-licensed advisor understands which investments a US person needs to avoid if they are living in Canada. Some investments are considered PFIC's (Passive Foreign Investment Companies). Your cross-border financial advisor will be familiar with the pensions in Canada and the US and how to plan your retirement. They will help you to avoid the common, costly pitfalls of a cross-border move.

What is the Canadian Equivalent of a Roth IRA?

The Canadian equivalent of a Roth IRA is a TFSA. Although the plans have differences, there are significant similarities. A Roth IRA and a TFSA are funded with after-tax dollars, and the growth and income earned in the account can be free from taxation if the rules are followed. Neither plan has a required minimum distribution or a time when you must stop making contributions.

The main difference between a TFSA and a Roth IRA is the contribution rules. A TFSA has an annual amount set by the government that you can contribute as a Canadian resident. This contribution room can be carried forward and is independent of income. You can withdraw at any time, and you do not owe tax or penalties on the withdrawals.

With a Roth IRA, any distributed earnings have to be qualified to avoid penalties and taxation. You also need to have earned income to be eligible to contribute. If your income is too high, you will not be allowed to contribute.

The area of cross-border taxation and cross-border investing is complex and may seem overwhelming. Working with a qualified cross-border accountant and a cross-border financial advisor ensures you are on the right track, make the best decisions, and avoid overpaying tax.

Common Questions

Can I have a Roth IRA in Canada?

While you can keep an existing Roth IRA after moving to Canada, there are a few steps you need to take to ensure it isn’t considered a taxable account in Canada. In addition, you want to make sure you do not contribute to a Roth IRA as a Canadian tax resident. It's essential to consult with a cross-border financial advisor to navigate the rules and implications.

Can I maintain my US Roth IRA account while living in Canada?

Yes, you can maintain an existing US Roth IRA account while living in Canada, but you must file a one-time Treaty Election by the filing date to the CRA. There are tax implications if you don’t plan the account properly.

Can I open a Roth IRA as a Canadian resident?

Opening a Roth IRA as a Canadian resident does not make sense. It's advisable to seek guidance from a cross-border financial advisor to understand your options and compliance requirements.

Are my Roth IRA contributions eligible for tax deductions in Canada?

Roth IRA contributions are not tax-deductible in Canada. Additionally, earnings and withdrawals may have different tax treatments under Canadian law, so professional advice is recommended.

What are Tax-Free Savings Accounts (TFSAs) in Canada?

TFSAs allow Canadians to save and invest money tax-free, with contributions not being tax-deductible but withdrawals being tax-free. They offer flexible investment options and are a great tool for tax-efficient savings. Caution should be used as a US person living in Canada because a TFSA is not considered a tax-free account by the IRS.

What is a Registered Retirement Savings Plan (RRSP), and how does it work?

An RRSP is a Canadian retirement savings plan that provides tax-deferred growth on contributions and investment income. Contributions are tax-deductible, reducing your taxable income for the year, and withdrawals are taxed as regular income upon retirement.

What is a Registered Retirement Income Fund (RRIF)?

An RRIF is an account that converts your RRSP savings into retirement income, requiring you to withdraw a minimum amount each year. Withdrawals are taxed as income, similar to RRSP withdrawals, and it's a common way to manage retirement funds in Canada.

How does Canadian income tax affect my investments and retirement savings?

Canadian income tax impacts the growth and withdrawals of your investments and retirement savings, with tax-deferred accounts like RRSPs offering immediate tax benefits. Understanding tax rules can help optimize your savings strategy.

How can I lower my taxable income in Canada?

You can lower your taxable income by contributing to RRSPs, making use of tax deductions and credits, and optimizing your investment strategies. Charitable donations and certain eligible expenses can also help reduce your taxable income.

What are the benefits of the tax deduction on RRSP contributions?

RRSP contributions reduce your taxable income for the year, providing immediate tax relief. This encourages saving for retirement while offering a tax-efficient growth environment for your investments.

What are the benefits of a Tax-Free Savings Account in Canada?

TFSAs provide tax-free growth and withdrawals, offering flexibility for various financial goals. They complement other retirement and savings plans by providing a tax-efficient way to grow your wealth. Caution should be used if you are a US person because the IRS views a TFSA differently.

Why should I look beyond tax-free savings accounts when planning my retirement?

There is a limit to how much you can contribute to a TFSA, and you will need to explore other options. A comprehensive retirement strategy includes tax-deferred growth options like RRSPs and other tax-efficient investment vehicles. Diversification can enhance your overall retirement savings.

What steps do I need to take to open a Tax-Free Savings Account in Canada?

To open a TFSA, you need to be a Canadian resident, have an accumulated room, have a Social Insurance Number (SIN), and meet the age requirement. You accumulate room in a TFSA every year you are a Canadian resident over the age of 18 starting in 2009. You can open a TFSA through various financial institutions, including banks and credit unions.

How does a High-Interest Savings Account compare to other savings options in Canada?

A High-Interest Savings Account offers higher interest rates than regular savings accounts, providing better returns on deposits. It's a secure and accessible option for short-term savings needs.

How do I choose a savings account in Canada?

Choosing a savings account in Canada involves comparing interest rates, fees, accessibility, and additional features. High-interest savings accounts typically offer better returns but may have more restrictions.

Summary of Key Points:

- You don't need to collapse your Roth IRA when moving to Canada.

- You should not contribute to your Roth IRA once you are a Canadian resident.

- Remember to file a one-time Treaty Election to the CRA by the filing date.

- Working with a cross-border financial advisor allows you to keep the Roth IRA.

- A cross-border accountant can help advise you on your taxable situation.

- It may not be best to convert an IRA to a Roth IRA while you’re a Canadian resident.

Next Steps

If you’re planning a cross-border move or you’ve already moved from the US to Canada and need help simplifying and optimizing your finances, then please get in touch. At SWAN Wealth, we specialize in cross-border financial planning and wealth management. We would be happy to ensure that you’re onside with the IRS while protecting your investments and retirement assets.

More Canadian and Cross-Border Financial Planning Articles & Guides

If you’re planning a move across the border or you’re already in Canada, these articles and guides will help you simplify and optimize your financial planning and make sure you’ve got everything covered.

The Ultimate Financial Planning Resource for Dual Citizens or Green Card Holders Living in Canada

Retiring to Canada - A Financial Planning Guide

Financial and Tax Planning for US Citizens Living in Canada

Canadian RRSP Facts for Dual Citizens, Expats and Canadians

About the Authors

Tiffany Woodfield is a dual-licensed financial advisor and the co-founder of SWAN Wealth Management, along with her husband, John Woodfield. Tiffany specializes in advising clients who live both in Canada and the United States and need to simplify their cross-border financial plan, move their assets across the border, and optimize their investments so they can minimize their tax burden. Together Tiffany and John Woodfield, CFP and Portfolio Manager, help their clients simplify their cross-border finances and create long-term revenue streams that will keep their assets safe whether they live in Canada or the US. Click here to schedule an introductory call with SWAN Wealth Management.

![]()